Scenario: Dad had a stroke. He can’t speak. To complicate matters, this happened while he was on a business trip in another state and he is in an HMO. Daughter needs to find out information from the health insurance company about where he can go for skilled nursing/rehab care after discharge from the hospital. Daughter calls insurance company and, of course, they don’t want to speak to her because there is no authorization form on file (and to get one on file can take 2 weeks for processing). The customer service representative will speak to the daughter if her dad gets on the phone, provides his contact information, and gives verbal permission… but daughter had already told representative that HER DAD CAN’T SPEAK as a result of the stroke. How could this inconvenience and aggravation have been avoided? By having a release of information form completed and on file. Take the time this weekend to print out your health insurer’s “Authorization to Release Information” form, fill it out, and send it in. Then call your insurer in two weeks and make sure they received it.

Here are links to the forms for some health insurers: Blue Cross and Blue Shield of Illinois United Healthcare Aetna Humana Medicare While this is not the most exciting topic, it is incredibly important and could save you some hassle in a crisis situation. Also, a reminder that when you call your health insurer, always keep detailed notes from the call and ask for the representative’s name and the reference number for the call. This could come in handy if there’s a dispute later about what you were told.  Holidays are often a time when we see family we may not have seen in a while. This may be even more true this year after dealing with Covid for the past 20 months. You may notice physical or cognitive declines in older family members. Be sure to take note of these changes and thoughtfully raise issues of health, safety, and living situation if it’s warranted. While we like to think of the holidays as a time to relax and catch up, they also offer an opportunity to take care of important health and financial planning. Here are some things that are important to have put in order before there is a health crisis:

I know that sounds like a lot to do, But if and when the time comes, you’ll be happy that you’ve done all this prep work! Please contact me if I can help with anything.  My kids always talk about how they didn’t learn practical stuff in school - such as how to file their taxes. This summer, I saw the perfect sign in a store: “Good thing I learned about parallelograms in school instead of how to do my taxes. That really comes in handy during parallelogram season!” I modified the sign a bit in the photo to the left. I wish there was a required class to learn about health insurance and Medicare! It sure would make open enrollment season a lot easier for health care consumers!

Some of the calls/emails I’ve received in the past few weeks:

Answers:

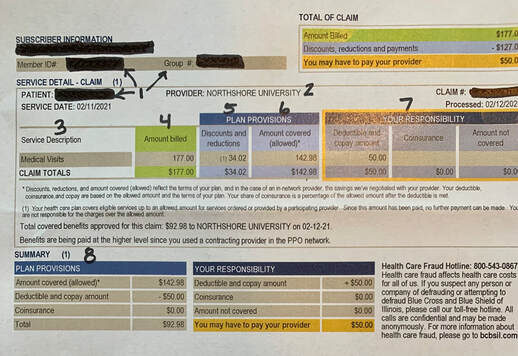

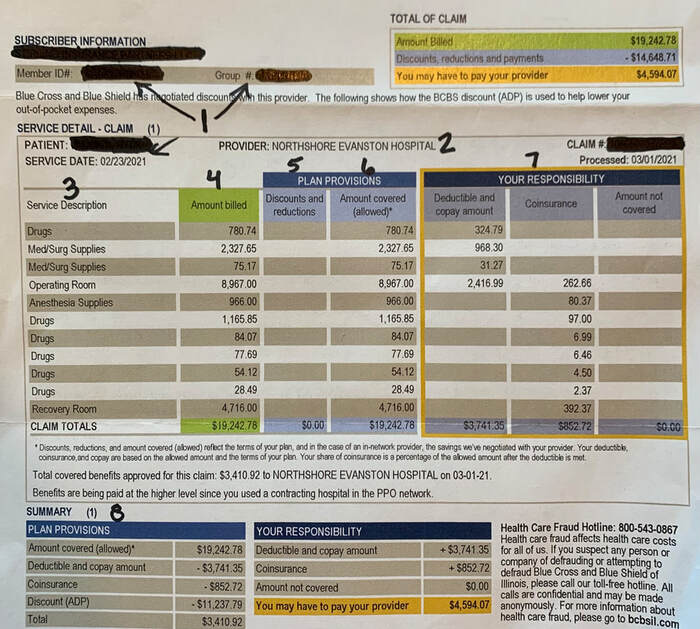

I can’t stress enough how important it is to take some time to learn about how your health insurance works and how Medicare works! A few tips about using your health insurance: #1 STAY IN-NETWORK. That’s pretty clear. Know your network. Choose doctors and hospitals that are in the network. Don’t rely on the online provider directory from your health insurer’s website - those are notoriously out-of-date and filled with errors. Call your provider to confirm and call the health insurer to confirm. Take notes about who you spoke with and ask for a reference number for the call to the insurance company. #2 Look over the plan documents and understand what’s covered, what isn’t, and what your costs are in different situations - e.g., going to immediate care vs. the emergency department. #3. Generics can save you money on prescriptions. #4. Make sure you understand the rules for pre-authorization. Err on the side of caution: call your health insurance company to confirm even if your provider tells you you don’t need pre-authorization or they took care of it for you. #5. When a test or procedure is recommended, ask questions. Why do I need this? What will it cost? What information will it give you that you don’t already have? Imaging tests (e.g., MRIs, CT scans) are generally most expensive in the hospital versus an outpatient facility. #6. For elective tests and procedures, be strategic about when you get them - before or after the new year depending on whether you have met your deductible or not. Specific to Medicare: #1. DO NOT switch plans - or switch from Original Medicare to Medicare Advantage - without having someone you trust look over the information. While you can switch between Original Medicare and Medicare Advantage each fall during open enrollment, you may not have “guaranteed issues rights” to get a supplemental policy at that time or at a later date. Tell everyone you know who is on Medicare not to switch plans without careful consideration and a second opinion from a family member or friend (or patient advocate!) #2. Medicare does not pay for long-term care. Period. It will pay for UP TO 100 days in skilled nursing/rehab in specific situations. After that, you’re on your own. #3. Medicare’s annual fall open enrollment season starts October 15th. The commercials, mailings, etc from insurance companies/agents are about to ramp up exponentially. Remember: if something sounds too good to be true, it usually is. Please do not make any changes to your Medicare without reviewing your options with someone you trust - some changes have lifetime ramifications! There’s so much to know about Medicare. I have a great presentation which helps people to understand their Medicare coverage. Contact me to schedule this presentation for your organization or even for a group of your friends. Bottom line: We aren’t taught about health insurance in school or anywhere else. It’s up to us to learn how the system works. But you still need to understand parallelograms to pass geometry.  Has ANYONE ever looked at an EOB (Explanation of Benefits) and thought “oh, this is easy to understand?” I bet very few people would say that. EOBs are definitely not written in plain language. There are codes, there are a bunch of numbers in different categories, sometimes the numbers do not even add up correctly. When you try to compare it to the billing statement from your health care provider, the terms used aren’t identical and the billing statement generally has very limited detail. How do you know if your claim was processed correctly and if you are paying the right amount? Estimates are that up to 80% of medical bills have an error. Therefore, it’s important to look at your bills and your EOBs and make sure that everything is correct. Also, know that an EOB is NOT a bill. Wait to receive a bill from your provider before making any payment. But be sure to look at the EOB before paying the bill. Here’s an example of an EOB (with identifying information blacked out):

Make sense???

Bottom line: Compare your EOB and billing statements; request an itemized billing statement from your provider. If you have questions, call the customer service number listed on the EOB or the back of your health insurance card. I’m happy to help as well!  A few months ago, my friend’s daughter, a freshman in college, had a health scare. Fortunately, everything turned out okay! But my friend hadn’t had her daughter fill out any of the necessary forms to allow the doctor and hospital to release information to her or even to speak to her about her daughter’s medical concerns. Trying to get a busy (and uninterested) college student to fill out the necessary forms while in another state in the middle of a semester was not quick, easy, or painless.

There are privacy laws (HIPAA) that restrict what a health care provider can share about any adult 18 years or older. Yes, this applies even if your adult child is still on your health insurance plan. Please refer to this article with advice about what forms you should have your 18+ year-olds sign. You can complete these forms on your own or meet with an estate planning attorney. (Special thanks to Emily Rozwadowski of Spencer & Rozwadowski, LLP for reviewing this information.) Briefly, the four important documents are:

If your adult child is attending college in another state, it may be safest to fill out forms for each state. Some colleges have their own forms as well (e.g., the University of Illinois has this authorization to release confidential health information form); this is something worth asking about at parent orientation. Once you’ve filled out the forms, keep them in a secure place. Also, be sure to scan them so you can easily access them from your phone as well as from your child’s phone. So, while you’re checking towels, sheets, comforter, etc off of your college packing/to do list this summer, please add “fill out important forms!"  I’m still bothered by a conversation I had last month with a hospitalist (a hospital-based doctor) at a prominent hospital in the Chicago area. I was speaking to him on behalf of a client’s family members who were already very frustrated. Repeatedly during the 10 minute conversation, he said that he had done all he could for the patient “given the constraints of insurance.” I finally asked him what he would do for the patient if there weren’t any insurance constraints. Frankly, he stammered and gave a lame response. We all know that insurance and other financial incentives drive many health care decisions, but for a doctor to flat out, dispassionately admit to a private patient advocate that insurance was what was driving his medical decision-making? It was shocking.

The sad reality is that this happens all the time in our healthcare system. Insurers - private as well as Medicare and Medicaid - make decisions about what treatments they will cover, how long a patient can be covered in a hospital or skilled nursing facility, what medication can be prescribed, and more. Some of the common ways this is done is through prior authorization for procedures and step therapy for medication. Note that the decision of an insurer not to cover something doesn’t mean you can’t get it, it means that your insurance company will not pay for it. Yet the reality is that most people cannot afford to self-pay for expensive treatments. What can you do about this? Know your insurance policy. Your insurance policy is a contract between you and the insurer. Of course it’s a unilateral contract that you have no ability to change - or even look at before enrolling, but it is a contract. It’s not fun reading, but you should know what it says. Use the language from the policy to make your argument for why something should be covered. Know what your rights are as a patient. The American Medical Association (AMA) has published physician and patient rights and responsibilities. Medicare beneficiaries have legal rights, including related to hospital discharge. Most major healthcare organizations have their own set of patient rights and responsibilities; you should be able to find this online. I recently worked with a family and the case manager at the facility was giving them the run-around about setting up a family meeting with the physician; after some back and forth, I ended up quoting directly from the facility’s patient rights document and - like magic! - a Zoom meeting was set up for later that afternoon. Be persistent. I like to say that insurance companies are bigger and badder than us and are counting on us to feel overwhelmed, intimidated, and just give up. Stick with it. Know the facts: what does your policy say; what is considered best practice and what peer-reviewed evidence is there; what are your rights as a patient/member. Advocate for yourself. Use the above tips to advocate for yourself or a family member. Be polite but firm and persistent. Enlist the assistance of your healthcare providers. Go up the chain of command. Please contact me if I can help Last spring, when I first wrote about navigating the health care system during the restrictions due to Covid, I never thought I would still be speaking and writing about that topic now! But it’s still extremely relevant as visitor restrictions are still in place for inpatients, patients in emergency departments, outpatients, and long-term care residents. I spoke on this topic recently as part of the North Suburban YMCA’s Adult Education Series. Basically, the guidance to be prepared and focus on good communication applies more than ever. The video also includes tips regarding telehealth appointments. Regarding being prepared, think about these two questions:

I’ve blogged before about the importance of creating a health information binder. It’s critical to do so AND to make sure that someone knows where it is so they can access the important information and advocate for you. Communication is different as you may have to rely on phone and video communication when your loved one is in the hospital. Key points include:

Choosing the right health insurance plan can be overwhelming. It may be tempting to just keep the plan you currently have rather than look at spreadsheets and dense, hard-to-decipher descriptions of coverage options. That’s a mistake. Whether you’re over 65 and inundated with advertising about Medicare open enrollment options or getting your insurance through the Marketplace or working for a company whose annual open enrollment is taking place this fall, it’s imperative that we review our current plan and see what our options are for 2021.  Here are some things to keep in mind regardless of where you get your health insurance:

Medicare Medicare Open Enrollment started October 15 and you can’t watch TV these days without seeing commercial after commercial about different Medicare insurance options. During Medicare Open Enrollment you can:

A few tips:

Health Insurance Marketplace and Employer Health Plans

Bottom line: Be sure you understand your options, get your questions answered, and know your preferences (cost, access, convenience, willingness to accept risk, etc.) before you make a decision. Contact me if I can help answer questions or conduct an analysis for you. Medicare is complicated. There are a lot of “parts” as well as rules, enrollment periods, etc. I’ve started making 1-2 minute videos to explain different aspects of Medicare including what is open enrollment, what isn’t covered by Medicare, Parts A, B, and D, what is IRMAA, and more. I'll be adding to this "Medicare collection" periodically so subscribe to my YouTube channel to stay up to date.

|

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

February 2024

Categories |

RSS Feed

RSS Feed